The Finance Act for 2025 should be enacted and published in the Official Journal in the coming days.

Among other measures, it provides for the establishment of a Differential Contribution on High Incomes (DCHI) codified in Article 224 of the General Tax Code (GTC). This new contribution targets taxpayers with an adjusted reference taxable income for the year 2025 exceeding €250,000 for a single person and €500,000 for taxpayers subject to joint taxation.

Furthermore, taxpayers who are not tax residents of France are excluded from the scope of the DCHI.

A mechanism ensuring an average tax rate of at least 20%

This new contribution aims to set up a minimum tax rate of 20% on 2025 incomes. It corresponds to the difference (when positive) between 20% of the adjusted reference taxable income and the sum of income tax, the Exceptional Contribution on High Incomes (ECHI), and final withholding taxes due on 2025 incomes.

In other words, taxpayers whose effective tax rate in 2025 (income tax + ECHI + final withholding taxes) is higher than 20% of the adjusted reference taxable income will not be affected by this differential contribution.

An advance payment due in December 2025

The application of the DCHI is planned for the year 2025 only. However, it is important to note the French legislator’s tendency to make initially temporary contributions permanent, like the ECHI which has been in force since its introduction in 2011.

To circumvent the principle of non-retroactivity in tax law, the legislator has provided for an advance payment system equal to 95% of the contribution.

This advance payment will be payable between December 1 and 15, 2025, with the balance payable the following year. Penalties are provided to encourage a fair assessment of the advance payment.

Thus, a penalty of 20% is applicable:

- in case of failure or delay in payment of the advance;

- and when the advance payment is more than 20% lower than the amount that should have been paid (i.e., 95% of the DCHI finally due).

In the first case, the penalty base is 95% of the DCHI while in the second case, this base will be equivalent to the amount not paid through the advance.

Calculation of the DCHI

As a reminder, the Exceptional Contribution on High Incomes relies on the reference taxable income, which includes taxable income, deductions, tax credits and reductions, as well as certain exempt income and allowances.

The Differential Contribution on High Incomes, on the other hand, is based on the adjusted reference taxable income, which corresponds to the reference taxable income after certain adjustments. This adjusted reference taxable income is used both to determine the threshold for the contribution’s scope and as the calculation base.

A certain number of incomes exempt from income tax have been removed from the adjusted reference taxable income base, thereby excluding them from the DCHI’s scope.

These include the fixed €500,000 allowance on gains from the sale of securities by retiring managers, the 40% allowance on distributed income in case of election for the progressive scale, and the 50% allowance applicable to gains from free share allocations up to €300,000.

Products and incomes exempted by a bilateral tax treaty as well as those benefiting from income tax exemption under Article 155 B of the CGI (expatriate regime) are also excluded from the adjusted reference taxable income of the DCHI.

It is specified that incomes which, due to their nature, are not likely to be received annually and whose amount exceeds the average net incomes based on which the taxpayer was subject to income tax over the last three years, will be taken into account at 25% of their amount only.

This contribution aims to ensure a minimum taxation of the highest incomes at 20%, calculated according to the following formula:

The income tax, ECHI, and withholding taxes considered in this calculation are also subject to adjustments listed below:

The income tax considered corresponds to the basic rights:

- Increased by €1,500 per dependent and €12,500 for taxpayers subject to joint taxation;

- Increased by the benefit provided by a limited number of tax credits and reductions, such as tax credits provided by international tax treaties, the tax reductions of the Duflot and Pinel schemes, the tax reduction for cash subscriptions to the capital of companies, the reduction granted for expenses related to property restoration in protected sectors, etc.

The tax paid on exceptional incomes (themselves taken into account for 25% of their amount) will only be considered for 25%.

The ECHI, without applying the quotient mechanism intended to mitigate the taxation of exceptional incomes. Thus, the ECHI of a person who has benefited from the quotient system will be increased only for the purposes of calculating the DCHI. This ultimately preserves the benefit provided by the quotient mechanism.

The final withholding taxes paid after the publication of this Finance Act for 2025. Those paid before this date will not be taken into account, and correspondingly, the incomes they tax should not be included in the adjusted reference taxable income.

Furthermore, a mechanism has been instituted to limit the side effects when the adjusted reference taxable income, after adjustments, is between:

- €250,000 and €330,000 for single, widowed, separated, or divorced taxpayers; or

- €500,000 and €660,000 for taxpayers subject to joint taxation.

In this case, the amount corresponding to 20% of the adjusted reference taxable income would be reduced by the difference between:

- 20% x the adjusted reference taxable income; and

- 5% of the adjusted reference taxable income amount – €250,000 or €500,000 (depending on the household composition)

It is important to note that social contributions are not taken into account in the calculation. Thus, for capital gains or investment income subject to the “flat tax” of 30%, only the flat income tax of 12.8% is considered (the “flat tax” being composed of a flat income tax of 12.8% and social contributions of 17.2%).

First Example

Context

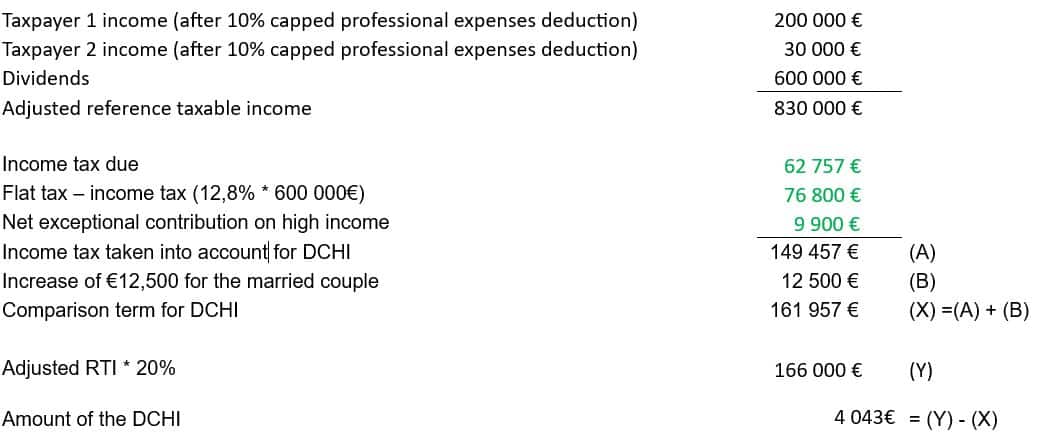

Mr. X is an entrepreneur at the head of a thriving SME in recent years. He pays himself a salary of €214,171, and his wife earns a taxable net salary of €33,333. After several years without paying himself dividends, he paid himself €400,000 last year to finance the purchase of a secondary residence to accommodate his children, who are no longer dependents. Considering the many underestimated renovation works, he would like to pay himself a supplementary dividend of €600,000 this year (i.e., 2025).

Analysis

First of all, it is crucial to examine the applicability of the DCHI. Indeed, it is undisputed that the €600,000 dividends exceed the average net incomes subject to income tax for the last three years.

However, several questions arise:

- Is this an “exceptional income by nature that is not likely to be collected annually”?

- Should the notion be derived from exceptional incomes benefiting from the quotient mechanism provided for in Article 163-0 A of the CGI?

- If applicable, is it mandatory to request the benefit of the quotient for income tax purposes to benefit from the derogatory regime allowing only 25% of the amount to be accounted for?

Scenario 1: The income is not considered as exceptional income under the DCHI

Mr. and Mrs. X will have to voluntarily pay an advance of DCHI amounting to €3,841 [(166,000 – 161,957) * 95%] between December 1 and 15, 2025.

If they fail to pay at least 80% of these 95% on time, a 20% penalty could be applied.

Therefore, their total tax liability would be:

Scenario 2: The income is considered exceptional under DCHI.

The adjusted reference taxable income is less than €500,000 for a married couple. Mr. and Mrs. X are thus outside the scope of the DCHI.

Second Example

Context

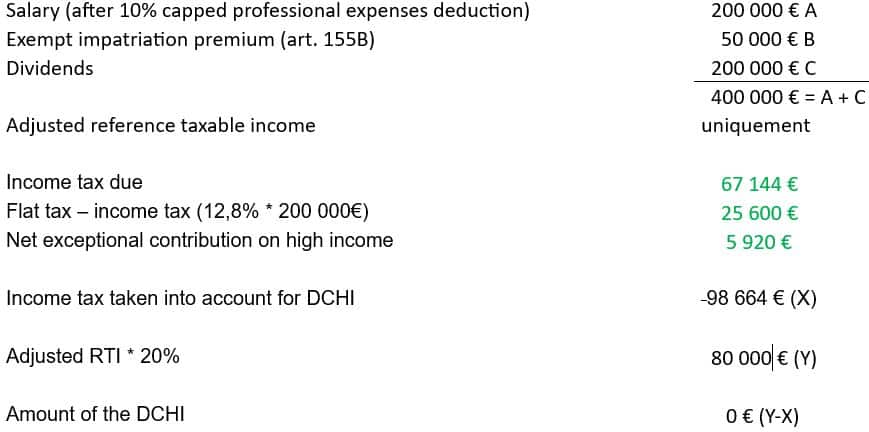

Mr. R is an employee benefiting from a €50,000 impatriatie premium exempt under Article 155B of the GTC (impatriate tax regime). He is divorced without dependent children. Aside from his net taxable professional income of €200,000, he has a very comfortable portfolio of listed shares in a French bank, inherited from his parents. This year, he receives €200,000 in dividends, slightly more than in previous years.

Although he is within the scope of the DCHI, the amount of tax paid considered in the calculation is above the minimum contribution. Therefore, no DCHI will be due.

His total taxation would then be: